I received a letter in the mail the other day, a nondescript white envelope from my credit card company. It was the sort of envelope I’d usually toss into the recycling figuring it just contained special offers on merchandise purchasable for all the points my wife and I have accumulated by using the card for 22 years. But uncharacteristically, I opened it.

The letter inside filled a full page, and in dry language explained that the interest rate charged on our card was being raised to 19.99% on January 1, 2010. It gave no explanation of the rate increase – poor payment history or if this was a change being made to all card holders, not just us. Further down the letter, it said we could “opt out” which means use the card at our current rate until it expires at which point it would not be reissued. It also offered, and here’s the blackmail part, a lower interest rate if we’d agree to spend a minimum of $1,500 per month and make payments on time. We have an “auto-pay” plan in place so paying on time is not an issue. But I was offended by the requirement that we spend $1,500 monthly.

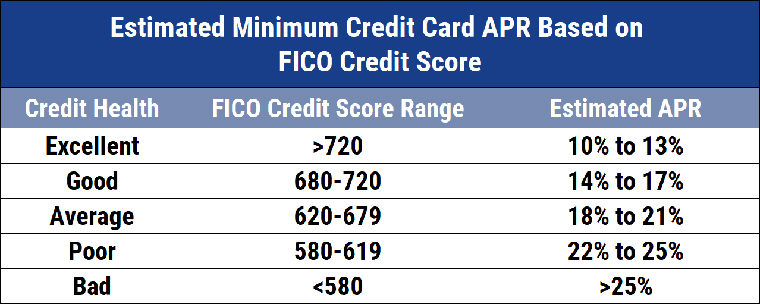

The credit card world, which is the world of banking, is morally upside down. Charging rates that 50 years ago would have subjected them to prosecution for usury (like 29.99% interest due to delinquency!), the banks and their credit cards use late fees and insane interest rates to lock people into perpetual debt. Now that many transactions require credit cards, people are virtually forced to use them. Those that pay them off completely each month are called “freeloaders” by the bankers, and this latest effort to secure high monthly purchases is a blatant attempt to force more people into debt.

I called my credit card company to ask them why my rate was being changed. A representative coldly stated that “the change was to enable the continuation of credit.” When I asked him if this was a card-wide change, he brusquely answered that he was “not going to feed any rumor mills,” and refused to tell me more. This is what 22 years of payments made on time earns you in 2010. Disgusted, we “opted out.”

I went to the local bank to find out what they offer, and approached a young man named Socrates at one of the desks. One has hope when one asks a person named Socrates a question, but he said that “all the credit card companies are doing the same thing.” Ah, well. Now that the big banks have been bailed out by us tax-payers our reward is 19.99% interest unless we pay ransom. Paying many millions to lobbyists to get congress to legalize usury is not expensive for banks when they can so easily pick our pockets.

The average American’s neck has been placed in a financial noose. During difficult times credit cards can buy a month or two of security while a new job is found, but the banks are playing on such hardship by tightening the noose. Just as the bank/mortgage industry had no compunctions about foreclosing houses instead of working with homeowners, the bank/credit card companies have no hesitation about yanking on the rope from which many now hang.